Gold Leads. Bitcoin Finishes.

AI Summary

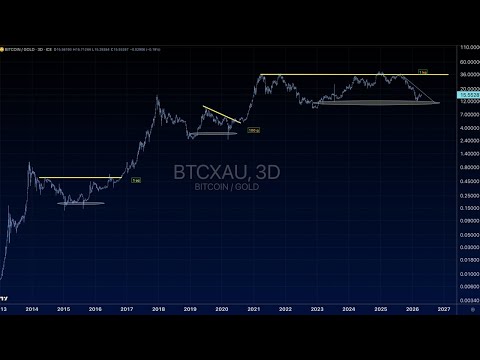

The discussion begins by highlighting gold's "super cycle" in 2023, noting its tremendous run and a period of consolidation, offering opportunities for dollar-cost averaging (DCA). The speaker draws parallels with past Bitcoin bear markets against gold, where gold's bull runs preceded significant Bitcoin bull markets. The first two Bitcoin bear markets saw 85% and 84% drawdowns, respectively, each followed by a retest of the low before a gold bull market led to a Bitcoin bull run. The most recent bear market, however, has different characteristics: it's longer in duration, with a diminished drawdown of 75%, and only 68% during Bitcoin's mega bull market. This is attributed to a fundamental shift where central banks have heavily invested in gold.

The conversation then shifts to the broader business cycle, acknowledging varying opinions. Some believe the cycle is ending, potentially manifesting as a "triple top" on the NASDAQ, especially if a major engulfing candle appears next week. Others, like Elon Musk and Kathy Wood, foresee substantial GDP increases and an "arc of epic proportions" for the business cycle after a period of suppression. The current market ascent, led by the "MAG7" (Magnificent Seven), has been incredible, with many money managers feeling "short" and under pressure to chase, which could lead to a "euphoric top" before a severe bear market. The rapid shift from extreme oversold to extreme overbought in many assets is unusual, with April historically being a volatile month.

Geopolitical developments are also discussed, specifically a 10-day ceasefire between Israel and Lebanon, seen as a concession from the U.S. side for Iran. Concerns remain about Iran's posturing regarding toll charges for the Strait, currently under U.S. blockade. The speaker warns that a positive situation could quickly unravel, potentially reaccelerating oil prices above $120, which would significantly pressure global and American economies. Markets are currently pricing in a resolution, with future focus on the upcoming Trump-Xi meeting and corporate earnings.

The speaker emphasizes the importance of market resilience, noting that many were not expecting new equity market highs a week after significant events. The potential for hyperscalers to pull back on data center construction is highlighted as a "red flag" that could end the current market run. Conversely, large IPOs and increased CapEx spending by companies like Anthropic and SpaceX could fuel further growth.

Regarding investment positioning, the speaker addresses the development of a new trading system, "V4," which is the highest priority for community release. Current forward tests show a long position bias, with GBTC (Bitcoin play) and MicroStrategy confirming long positions, indicating a return of upside momentum after four months. NVIDIA also holds a good long entry.

A specific question from a user named Brian regarding managing stock trades, particularly Tesla, is addressed. Tesla, and NVIDIA, are noted for having very tight stop losses on the "V2" system, leading to a low win percentage (30% for Tesla) but a massive 14-to-1 risk-to-reward ratio (average winning trade 27% vs. average losing trade less than 2%). This means investors should expect to be stopped out on 70% of Tesla trades, but the profitable ones offer substantial gains. The speaker shares a personal example of a 46% gain on Tesla in November that absorbed previous losses.

Another user's experience with "V4 buy-side boost" is discussed, noting four consecutive losses. The speaker explains that such strings of losses are "extremely common" even with a 48% profitable rate and a 5-to-1 risk-to-reward ratio for buy-side boost (average winning trade 13% vs. average losing trade 2.5%). Historical data shows similar periods of multiple consecutive losses and extended flatlining in Bitcoin's price action, particularly reminiscent of 2018. The speaker advises that investors must have realistic expectations about win/loss ratios and risk-to-reward, and consider whether to trade only in defined bull markets, such as those identified by Bitcoin's bull runs. The recent "battle-tested" period of flat price action is seen as beneficial, as it suggests that future trades are likely to revert to the average profitability, potentially bringing up overall performance.