Central Banks, Big Tech, and a Market at the Edge

AI Summary

The speaker begins by highlighting a significant week ahead, with central bank activities and a focus on the US dollar and Japanese yen. The yen is trading just below 160, and its future strength depends on whether the Bank of Japan hikes rates in May to 1% or delays. This is crucial as the yen's unwinding has caused market turbulence, a topic previously discussed in December 2023.

The speaker then shifts to their weekend work, having spent 14 hours on Ethereum, specifically reviewing their V4 crypto models. This intensive focus on crypto follows the completion of V4 models for stocks, signaling a return to re-evaluating Bitcoin and crypto strategies. The goal is to avoid complacency and continuously refine their approach.

The presentation starts with the V4 stock models. The speaker mentions the release of these models to the community, with updates to follow as further gains are made. They start by comparing the V2 TQQQ template with the V4, showing significant improvements in drawdown and overall return, particularly from 2019. Further refinements led to minor improvements, reducing drawdown and slightly increasing overall return, both described as "fantastic."

A recent discussion with a colleague, B South, is recounted, where a 94% CAGR with less than 7% max drawdown was initially presented for Ethereum. However, upon removing MicroStrategy and GBTC, the CAGR for TQQ, NVIDIA, and Tesla was 74% with a 6% drawdown. The speaker believes they can still make incremental gains, demonstrating this with TQQ.

Next, Tesla's performance is reviewed. The V4 shows massive performance, with a 23% return. The speaker emphasizes the improved equity curve and a more than halved drawdown, which is a significant achievement. They acknowledge a dilemma regarding Tesla's V4, as there are two versions with different drawdowns (11% vs. a much lower one) and profit factors. They consider releasing both V4 A and B for community testing or analyzing year-over-year consistency to determine the better option.

GBTC is then discussed, comparing the current V2 template with the new release. The drawdown remains similar, but overall profitability and profitable trades show improvement. The speaker notes having two versions for GBTC as well, one with a higher drawdown and lower profitability but higher total P&L.

A question arises about the potential for overfitting or "curve fitting" in these models. The speaker clarifies that the concern is not about curve fitting but rather about whether the models are poorly or well-designed. They highlight that their models are forward-tested, and a "zero filter" version was created for this purpose. While zero-filter versions showed slight outperformance, the filtered versions demonstrated true performance. The speaker stresses that each asset has its own structure, and good modeling is key, with money management added to the V2 templates as a significant differentiator.

Returning to GBTC, the speaker confirms having A and B versions. They then compare "Sorrentino" and "Sharpervich" models, noting a "massively better" performance for Sorrentino in one instance (3.2 vs. 2.1 and 1.25). They examine the profit factor and drawdown differences, observing that one version trades more frequently.

FNGD is brought up, with the speaker speculating whether "Bulls" might replace it. FNGD, the inverse of FNGU, had a data switch in 2025. The speaker notes a good template for FNGD with recent small changes and improvements. They then compare it to "Bulls," which has less data (covering the last three years) but shows a fantastic CAGR and a higher win ratio (55% for Bulls vs. lower for FNGD). The speaker leans towards Bulls but acknowledges the need for further analysis.

NVIDIA's V2 template is presented as a strong performer, currently yielding a 17% return. The V4 shows improved drawdown and profitable percentage. The speaker emphasizes the importance of these models in retirement planning, citing Charlie Munger's perspective on the risk of market crashes when withdrawing funds. The models aim to provide consistency and reduce drawdown, which is crucial for long-term financial stability.

The "Strategy" template is highlighted as their best performer in 2025, holding an 18% return with good volatility management. The V4 version shows solid improvements in drawdown.

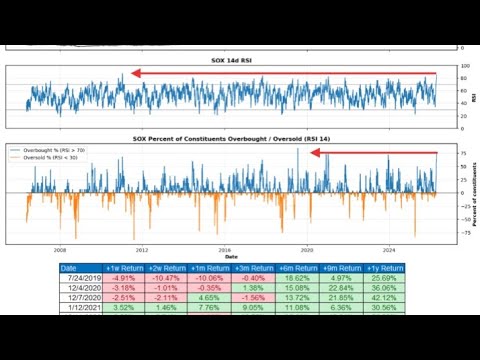

SOXL is mentioned as the only missing piece from the current puzzle, which the speaker is holding off on due to its current "moonshot" status. They sold their CHPY last week, noting its 4% gain. The discussion then turns to the SOX index (not leveraged SOXL), which has seen 18 consecutive sessions of rallies, a rare occurrence. Historically, while the immediate three months after such rallies can be volatile, the six-month to one-year outlook has been "tremendously bullish."

The upcoming week is significant for earnings, with MAG7 companies (Amazon, Microsoft, Meta, Google) reporting on Wednesday and Apple on Thursday. The speaker focuses on their spending on compute, energy needs for competition, and potential changes in spending. They also mention the potential market impact of companies like Anthropik going public. SOXL is not yet modeled, but the speaker acknowledges the need to incorporate it and SOXS (for the short side) into their cadence.

The speaker then returns to Bitcoin and crypto, describing the past few months (late February through April) as the "most difficult regime" for their trading style, comparable only to 2018 before a 50% dump. They reveal having spent 14 hours on a new Bitcoin/crypto model, emphasizing the need to adapt to current price action. The V4 stock templates are prioritized for release, but the speaker expresses the need for the best V4 templates for Bitcoin and crypto as well. They also mention the desire for a universal template for assets showing "blow-off top" patterns, using a ticker "Car" as an example.

Comparing two Bitcoin models, they note they are "almost identical in performance" but act very differently, with one having 214 trades since 2018 and the other 1250. Despite the difference in trade count, profitable trades, drawdown, and return are very close, even with high commissions (0.1% on Bitcoin). The speaker highlights a significant improvement in drawdown, from 38% to 20%, in the newer version, calling it "much more attractive." This is a preliminary result from only 14 hours of work.

The speaker then clarifies that one of the discussed models is using only RSI 2 with no CTM filter, essentially a filter-less version. They also mention a new "table view" for their data. A key finding is that the "buy-side is superior, but the short-side is also superior to the other." They plan to address the high drawdown on the short side of one version.

The current market situation sees Bitcoin getting "hammered," with no clear narrative for the pressure. The speaker focuses on their building efforts. They note that markets have been "spectacular" ahead of earnings, with participants split. They mention rumors of funds moving to Wintermute and Binance, possibly indicating market shakeups.

Geopolitical events are also discussed, with the US claiming Iran is days away from having to shut off oil wells, causing permanent damage. Iran, in response, proposes opening the strait and maintaining a ceasefire. The speaker anticipates the blockade will continue and its effectiveness as leverage will be tested.

The upcoming FOMC meeting is mentioned, with the speaker expressing strong disapproval of Jerome Powell's tenure, accusing him of reckless money printing and causing damage. They believe the main event is the Bank of Japan's positioning and the MAG7 earnings, questioning whether the market will sell off after its recent run or if earnings will act as a catalyst for further gains. They criticize Janet Yellen and Powell for their handling of the economy, calling it the "greatest financial blunder of all time."

In conclusion, the immediate next step is to release the polished V4 stock templates on a daily basis, including Tesla and GBTC. NVIDIA and Strategy are currently performing well, with 17% and 18% returns respectively. The speaker emphasizes their continued "grind and push" to deliver these tools.