This Is How Parabolic Bull Markets End

AI Summary

The market outlook remains uncertain, with several key factors influencing potential future movements. Yesterday's session saw the "mag seven" earnings, which provided significant insights, and the upcoming weekend holds the potential for further escalation in crude oil prices above $120 or a negotiated arrangement. Federal Reserve Chair Powell suggested a 30 to 60-day timeline to assess whether the recent energy price shock is a temporary event that the resilient economy can absorb, or if it will lead to significant, long-lasting macroeconomic consequences.

Bitcoin is currently undergoing a retest after a massive breakout attempt. While a green day for Bitcoin is welcome, a sustained move above the resistance level is necessary for confidence that a bottom is in. The current situation is described as a breakout retest, and confirmation of the retest and subsequent upward movement is crucial. A breakdown and subsequent retest scenario is also being monitored, where a resumption of the downward trend would confirm the retest of a previous low. Historically, gold bull markets have preceded Bitcoin bull markets, and a confirmed retest of a bear market low in Bitcoin against gold could signal a stronger probability of a market bottom.

Intervention in the Japanese yen by the Bank of Japan to strengthen the currency is a developing situation. The yen fell into a trendline after the intervention, raising questions about the effectiveness and sustainability of such actions. The critical $160 level for the yen was previously a point of verbal intervention, but the Bank of Japan has now moved to actual buying of yen. The potential for further market action, a break of the trendline, and its implications for market positioning and carry are being watched. If the $160 level is lost, the speed of the yen's devaluation is a key concern. A potential tightening by the Bank of Japan, with rates moving above 1%, could alter the landscape, but currently, it appears to be a struggle. Japan's energy dependence, exacerbated by the situation in Iran, is not aiding its position.

Crude oil prices are being influenced by contract rollovers, but the significant developments are expected over the weekend, dependent on whether selected strikes or actual negotiations occur regarding the situation in Iran. The coming weekend is viewed as pivotal.

The NASDAQ is being watched on a weekly chart. A concerning sign would be new all-time highs being faded, potentially signaled by a bearish engulfing pattern.

Regarding CapEx spending, Google's earnings were spectacular, with planned CapEx increases from $180 billion to $190 billion. Microsoft plans to spend $190 billion, and Amazon approximately $200 billion. Meta is seeking to raise $25 billion and plans to spend $145 billion. Combined, these four companies are projected to spend around $660 billion in one year. The potential IPO of Anthropic and the compute secured by OpenAI, sufficient for their expectations until 2029, are also significant factors. Despite a dip in NVIDIA's stock, there are no signs of companies pulling back on spending, and the race to invest in AI appears to be intensifying.

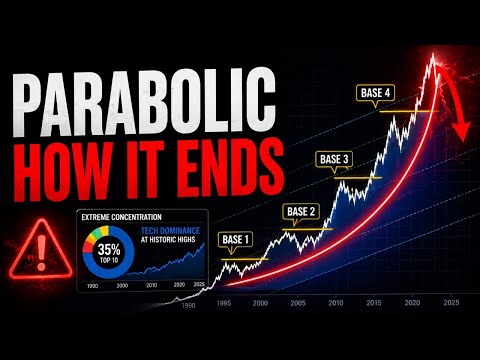

The impact of AI on productivity and economic growth is a central theme. While some express concerns about the return on investment for this massive spending, others highlight the potential for AI to drive further growth, especially with the impending automation of humanoids and robotaxis. The comparison to the dot-com bubble is drawn, but a key difference noted is that the "mag seven" companies are generating substantial earnings, unlike many companies during the dot-com era. However, concerns about concentrated risk in the market, particularly in AI, are valid, with AI currently representing a 41% concentration, similar to previous periods of high concentration like the Nifty 50 or the tech and telecom boom. The sustainability of this trend is linked to continued earnings generation.

Historical market movements, such as the massive run-up before the Great Depression and the tech-driven bull markets, are being referenced. Stanley Druckenmiller's past prediction of a "lost decade" has not materialized, and there is ongoing discussion about a potential sideways market. The importance of market timing, especially for those nearing retirement, is emphasized, referencing the opportunities and pitfalls of the 2000-2010 period. The financial crisis of 2008 and its impact on millennials, including a distrust of the federal banking system, is also discussed.

The current market sentiment is characterized by a mix of caution and concern. Concentration risk in AI is a significant factor, alongside the question of whether companies can achieve a return on their substantial AI investments. The analogy of the internet's transformative impact during the dot-com era is used to describe the potential of AI, but the time lag between investment and realized returns is a critical consideration. Companies like Meta are seen as adapting to future technological shifts, even if past ventures like the metaverse were not immediately successful. The massive spending on AI is viewed as a necessary step for long-term survival and relevance.

The potential for long-term yields to derail the current market is noted, particularly if crude oil prices continue to elevate. The possibility of crude oil trading above $120 or back down to $80 highlights the current volatility and uncertainty. The discussion also touches upon the perceived injustice of the financial system, particularly following the 2008 crisis, and the lasting impact on generational perspectives. The conversation concludes with an emphasis on adapting and staying ahead of future trends, acknowledging the significant consequences of both missing out on potential upside and being left behind.